Sector figures economic report spring

Cautious start to the new year

In the latest economic report from Swiss Textiles, the majority of companies in the Swiss textile and clothing industry assess the situation as neutral. Uncertainty prevails in general - particularly due to the unclear global customs situation. Trade figures, on the other hand, are developing favourably: With one exception, all sectors recorded growth. However, the outlook remains subdued - a consequence of the continuing volatility of the global economy.

What does Donald Trump's customs policy mean for Impact Acoustic? CEO Sven Erni talks to Swiss Textiles about trade barriers, China and the USA - and why he can still take something positive from the current situation.

After a positive start to the year, sentiment in both the sector and the Swiss economy as a whole deteriorated in the first quarter. However, the US tariff policy has not yet been fully reflected in the assessments, as some of the surveys were already completed at the beginning of April. The first negative trends are emerging, which are likely to intensify in the coming months.

In the manufacturing industry, too, prices are no longer expected to rise, but to stabilise.

Manufacturing industry

After the strong fluctuations in the previous year, the manufacturing industry has resumed its financial year with scepticism. The majority of companies surveyed take a neutral view of their situation. The order backlog improved compared to the turn of the year and was above the balance for the industry as a whole for the first time in a year. Nevertheless, the majority of companies still consider the volume of orders to be too low. The average capacity utilisation rate over the past three months is particularly worrying - it fell below 75% for the first time since the pandemic.

Wholesale

The assessment of textile wholesalers continues to recover from the slump in the previous year and is approaching the zero mark and the assessment of wholesalers as a whole - despite a slight drop in demand in the first quarter. Overall wholesaling also declined slightly: its balance was -16 points, while textile wholesaling was slightly lower at -20 points.

Retail trade

While the clothing retail sector was still sending out positive signals at the turn of the year, sentiment had cooled considerably by the end of the quarter. The balance of the assessment was -20 points and thus clearly below that of the retail trade as a whole. The latter assessed the situation as neutral. The main reason for the negative expectations was the significant decline in total sales over the past three months.

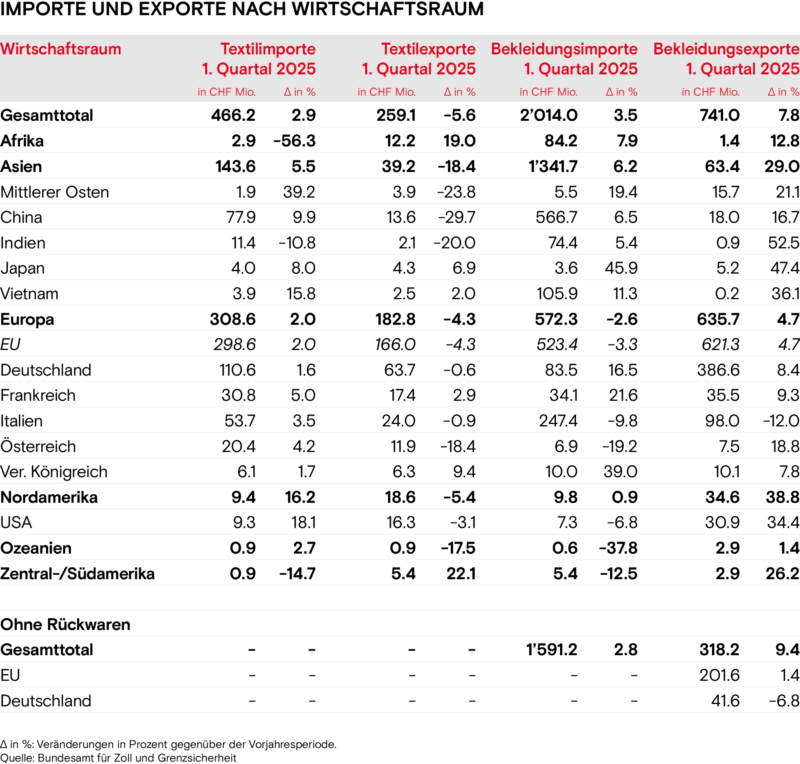

The EU's interest in Swiss textiles - still the most important sales market - is declining slightly. Nevertheless, it imported more clothing than in the previous year.

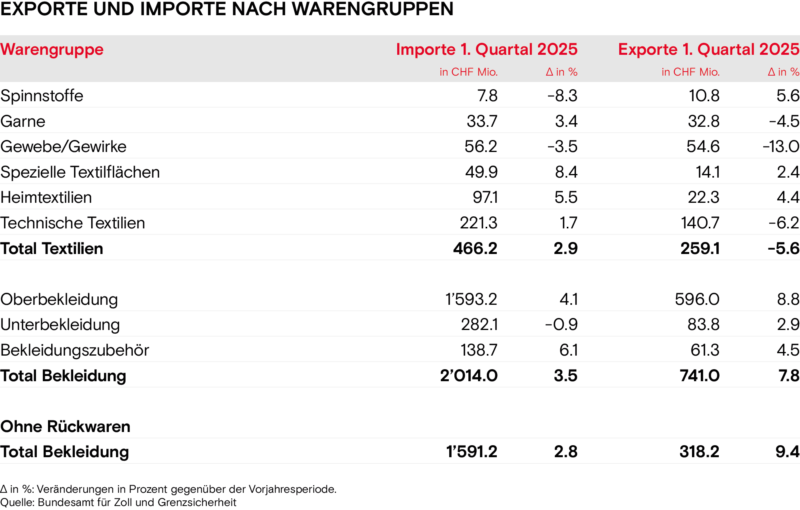

Foreign trade - focus on individual markets

While textile imports increased slightly in the new year, exports fell. The three most important export groups - yarns, woven and knitted fabrics and technical textiles - were particularly affected, suffering from a decline in interest. This is partly due to declining orders from China, the Middle East and the USA.

In contrast, imports and exports of clothing are clearly on the rise. Paradoxically, it is precisely these three markets that are growing noticeably in this area.

The EU's demand for Swiss textiles - still the most important sales market - is falling slightly. Nevertheless, it imported more clothing than in the previous year.

The strong growth in the USA is likely to reach its limits soon: While clothing exports were still up by 50 per cent in January, they more than halved in March to 22 per cent. Textile exports also declined. The ongoing tariff discussions are likely to exacerbate the negative developments.

Trade with China remains similarly volatile: textile imports in particular fluctuated significantly in the first three months.

Situation on the labour market

The unemployment rate in the manufacturing industry rose again compared to the previous year and stood at 3.4 per cent in March 2025. This puts it at the same level as the textile wholesale sector, where the rate remained stable at 3.3 per cent. Both figures are slightly above the national rate of 2.9 per cent.

Unemployment is likely to fall in the coming months, particularly in the wholesale sector, as the majority of companies surveyed expect employment to increase. The clothing retail sector and the manufacturing industry are more cautious. Both anticipate a minimal decline in employment figures.

This makes it all the more important to consistently improve the framework conditions and dismantle trade barriers wherever possible.

Outlook and expectations

While the expectations of the textile processing industry, the clothing retail trade and the economy as a whole are rather subdued, the majority of companies in the textile wholesale trade are expecting demand to grow. This assessment is also in line with the expected increase in employment. At the same time, a small majority of respondents expect sales prices to fall.

In the processing industry, too, prices are no longer expected to rise, but to stabilise. The export outlook remains subdued, as do the expected orders for the next three months.

The clothing retail sector is similarly sceptical: although sales are expected to rise slightly, the overall outlook remains cautious. A small majority of companies even anticipate a slight decline in the number of employees - not least due to the continued growth of Asian online markets.

Impending tariff war harms the economy

The tariffs announced by the US on 2 April are only partially reflected in the surveys. Nevertheless, the first two months since Donald Trump took office have already caused considerable uncertainty on many trade markets.

The numerous changes of direction in US customs policy and the threat of a trade conflict with China are likely to further increase this uncertainty. The situation is also causing problems for export-orientated sectors such as our Swiss textile and clothing industry.

This makes it all the more important to consistently improve the framework conditions and dismantle trade barriers wherever possible. The negotiations on the Bilateral Agreements III are a central basis. At the same time, the Federal Council must swiftly finalise the negotiations on the free trade agreement with Mercosur and ratify the agreements with India and Thailand.