Economic report autumn 2025

Economic stress test continues - political decisions necessary

In the latest economic report from Swiss Textiles, companies in the textile and clothing industry continue to assess the situation as challenging. The US tariffs are showing noticeable effects for the first time, while the recently announced tariff reductions are not yet included in the current results. The most important trading partner, the EU, also remains economically weakened. Only the Asian market is developing positively and offers a small ray of hope.

Trade has clearly felt the effects of the 39 per cent US tariffs introduced in August, as the latest figures show. Depending on the product sector, exports in August and September fell by up to 80 per cent compared to the previous year.

The deal that has now been announced comes at the right time.

Exports in the entire textile sector fell by almost 43 per cent in September - a hard blow for the industry. The deal that has now been announced therefore comes at the right time.

The clothing sector fell less sharply because many items are made up abroad and are therefore subject to a different rate of duty. Meanwhile, the retail trade appears to be easing somewhat.

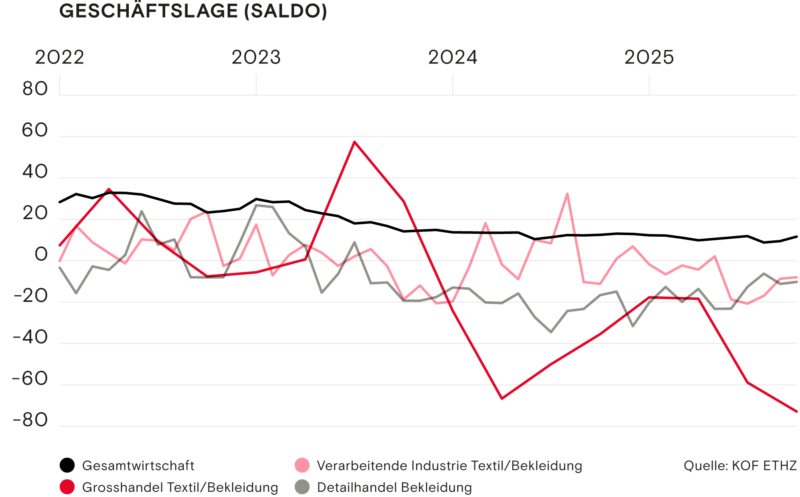

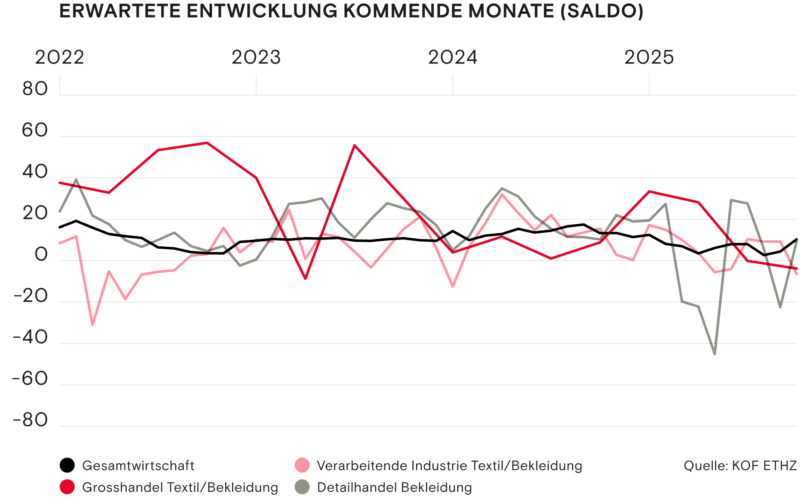

Manufacturing industry: slight recovery at a low level

After a weak summer, there are signs of a slight stabilisation in the manufacturing industry - albeit at a low level. Its capacity is being utilised at 76.1 percent, which means that it is slowly approaching the level of the industry as a whole. The business situation is also considered to be better than three months ago. Nevertheless, the balance remains negative. This is in line with the current order backlog, which a clear majority of respondents consider to be too low.

Wholesale: demand remains weak

Demand in the textile wholesale sector once again slumped significantly in the middle of the year. Although the trend in the third quarter is pointing slightly upwards, the balance remains in the red. This is also reflected in the current business situation, which remains very poor with a balance of minus 73 points.

Retail trade: cautious improvement

The clothing retail sector also had a difficult summer. The business situation in the third quarter remains negative. In a year-on-year comparison, however, the balance is above average - a cautiously positive sign.

The business situation represents the overall economic situation of the company. The test participants answer the question: "We currently rate the overall business situation as good, satisfactory or poor." The companies' expectations mentioned below are based on various questions about the expected business situation, order situation or turnover in the next three to six months. Here, too, there are three possible answers ("better", "neutral" and "worse"). Due to the slightly varying questions between the sectors, a direct comparison between the sectors is sometimes imprecise. However, the chart shows the trends in the coming months, which help with an assessment.

The seasonally adjusted balance of positive and negative responses is shown for the two indicators. This reflects the trend in development. In practice, the balances show a high correlation with the actual growth rates of the real indicators. The figures for positive and negative responses (percentages in the text) are not seasonally adjusted. (Source: KOF ETHZ)

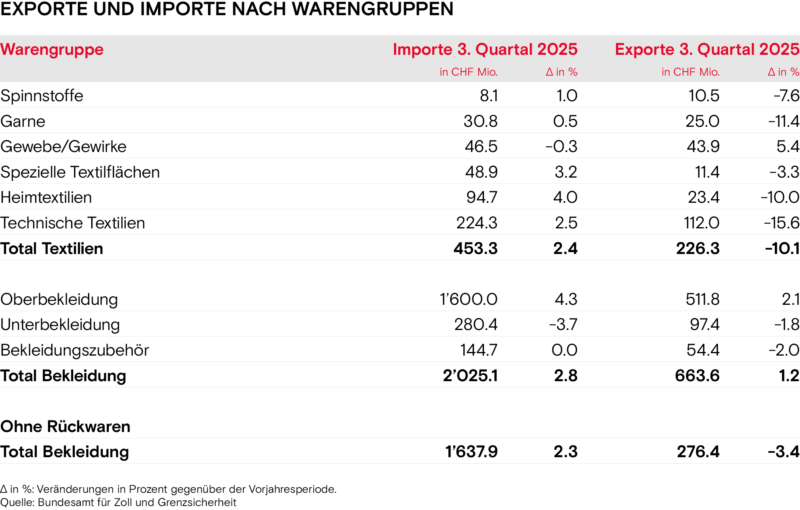

Foreign trade - focus on individual markets

The latest trade figures show how challenging the economic situation remains. Exports in both the textile and clothing sectors are down on the same quarter of the previous year. The decline in textiles is particularly marked at over ten per cent. On the import side, however, there is a slightly positive trend: both product groups increased by more than two per cent.

This development is gaining additional significance due to the Indian free trade agreement that has been in force since October.

Imports: Home textiles as a driver

With the exception of woven and knitted fabrics, textile imports increased in all product groups. Home textiles saw the strongest growth with an increase of four per cent. The two most important countries of origin, China and Germany, both recorded growth, albeit only minimal in Germany.

These are the first positive signals. China also remains a growth market in the export business. India is also one of the few countries with rising textile exports; in September, exports increased significantly by 165 per cent. This development is gaining additional significance due to the free trade agreement that has been in force since October.

This once again indicates a strong surge in the Chinese online markets.

Clothing: growing imports, declining exports

In the clothing segment, imports rose by 2.3 per cent, while exports fell by 3.4 per cent. China is the main driver of import growth. The large discrepancy between value and quantity is striking: while the value of goods increased by just under 36 per cent in the third quarter, the quantity imported grew by 145 per cent. This once again points to a strong surge in the Chinese online markets.

Trade with the EU, on the other hand, remains in decline; after deducting returned goods, exports fell by around 12 per cent.

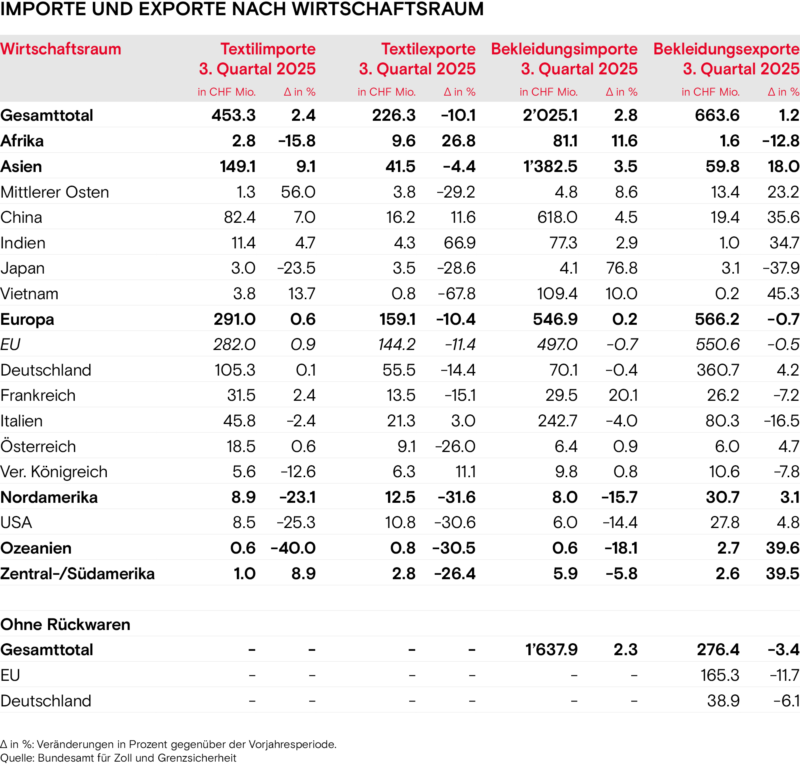

USA: the impact of tariffs clearly noticeable

The effects of the additional US tariffs of 39 per cent imposed at the beginning of August were evident in the first two months: textile exports slumped significantly, particularly in technical textiles and fabrics.

In the clothing sector, however, exports in September were 30 per cent higher than in the previous year. In August, they had fallen by seven per cent.

One reason for this is likely to be the different customs tariffs. Textiles - especially specialised technical products - originate from Swiss production and are subject to higher customs duties. Clothing, on the other hand, is usually manufactured abroad, which results in lower customs duties.

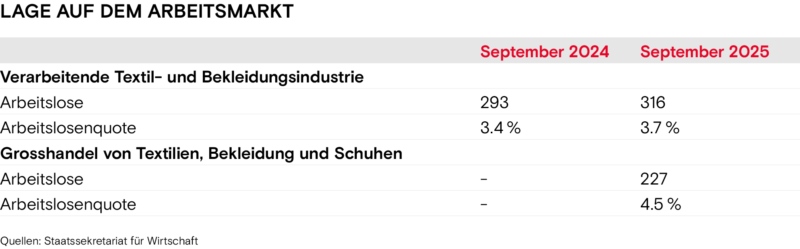

The labour market is proving more robust than expected.

Labour market proves resilient

The labour market is proving more robust than expected. There were fewer unemployed people than in the previous month, particularly in the manufacturing industry. Although the unemployment rate remains above the previous year's level, it stabilised slightly in September after rising over the summer months.

Wholesale: mixed developments

The situation in the wholesale sector is divided. While textile wholesaling is at a similar level to the manufacturing industry, the unemployment rate in clothing wholesaling is significantly higher than in previous months at 5.1 per cent. The sector exceeds the general unemployment rate of 2.8 per cent in September in all areas.

Rising rates expected

The unemployment rate in both the textile wholesale and manufacturing industries is likely to rise further in the coming months, as both sectors are expecting a decline in the number of employees.

Only in the clothing retail sector is the assessment somewhat more positive: With a balance of just under five points, it expects the number of people in employment to remain stable.

The export outlook remains subdued, as do the expected orders for the next three months.

Outlook and expectations

The clothing retail sector is the only one of the three sectors that is slightly positive. A small majority expect better months ahead. Its assessment of the situation is thus similar to that of the Swiss economy as a whole.

Textile wholesalers and the manufacturing industry have a small negative balance and are more cautious in their assessment of the situation.

Industry: stable prices, subdued expectations

The manufacturing industry is also no longer expecting prices to rise, but to stabilise. The export outlook remains subdued, as do the expected orders for the next three months.

While wholesalers are barely adjusting their expectations compared to the previous quarter, the manufacturing industry is anticipating a slight decline in orders and exports. This results in a negative balance of six points.

The economy needs better conditions

The Swiss textile and clothing industry remains under severe pressure. Demand in the EU and the USA has fallen, in some cases significantly, which is having a noticeable impact on many companies. Only the clothing retail trade and individual developments in Asia are somewhat more favourable.

Against this backdrop, the general economic conditions need to be improved:

- The recently announced 15 per cent tariff deal with the USA can contribute to this. Even if the new tariff rate is significantly higher than the previous year's figure and further measures are required. The equalisation with companies from the EU is particularly positive.

- In addition to the Bilaterals III, fair competitive conditions in the retail trade remain key for the sector. Foreign competitors continue to exploit regulatory loopholes via online marketplaces.

- The new free trade agreements with Mercosur and Thailand should also be ratified as soon as possible so that trade-based sectors can tap into additional markets.