Economic report summer 2025

Subdued mood in the first half of the year

After a subdued first quarter, the negative mood is now having a stronger impact. The Swiss textile and clothing industry is struggling with the poor global economic situation. This is despite the fact that the new US tariffs have not even taken full effect yet.

The economic and geopolitical environment is volatile. The same applies to companies' assessments, which have changed or darkened from the first to the second quarter. They were surveyed in June and July - i.e. before the decision on US tariffs was taken on 31 July. For export-orientated companies, the situation has once again deteriorated drastically. In addition to the sluggish global economy, Germany, an important partner, continues to face difficulties.

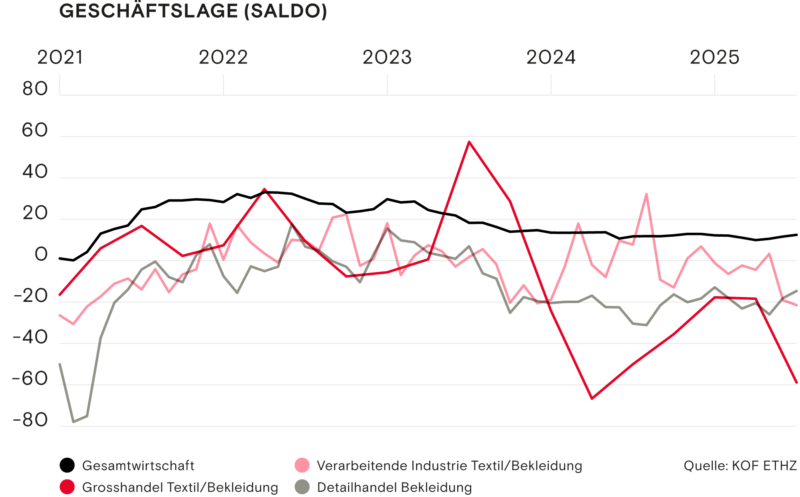

Manufacturing industry

The manufacturing industry again rated the business situation in the second quarter as gloomier than at the start of the year. The balance is now slightly below 20 minus points. Capacity utilisation showed a similar trend, at a good 75% it is well below that of Swiss industry as a whole.

The order backlog is even more extreme: at minus 64 points in the middle of the quarter, it was at its lowest level since the pandemic. In the current monthly survey, the value improved to just under minus 50 points. Nonetheless, the difficult phase in the textile and clothing manufacturing industry is clearly evident here.

Wholesale

An overwhelming majority of companies also rate the business situation in the textile wholesale trade as poor. The US tariffs are unsettling the market and causing demand to fall further in the second quarter.

Retail trade

The retail trade, which is largely dependent on domestic customers, is slightly more stable. Even if they are not in a buying mood, there are no signs of a downturn. The balance of the business situation remains at a level of just under 20 minus points.

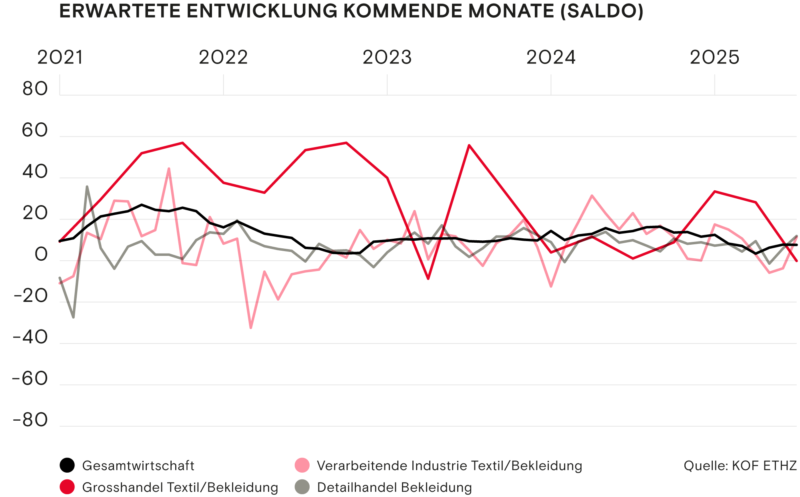

The business situation represents the overall economic situation of the company. The test participants answer the question: "We currently rate the overall business situation as good, satisfactory or poor." The companies' expectations mentioned below are based on various questions regarding the expected business situation, order situation or turnover in the next three to six months. Here, too, there are three possible answers ("better", "neutral" and "worse"). Due to the slightly varying questions between the sectors, a direct comparison between the sectors is sometimes imprecise. However, the chart shows the trends in the coming months, which help with an assessment.

The seasonally adjusted balance of positive and negative responses is shown for the two indicators. This reflects the trend in development. In practice, the balances show a high correlation with the actual growth rates of the real indicators. The figures for positive and negative responses (percentages in the text) are not seasonally adjusted. (Source: KOF ETHZ)

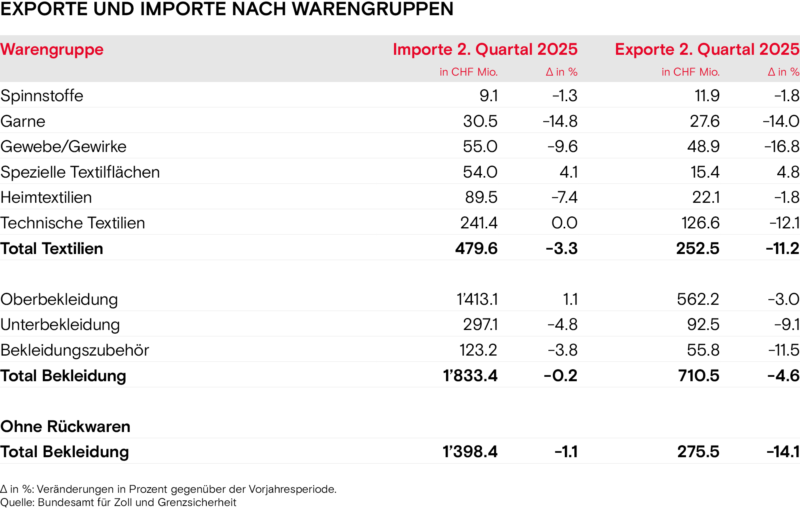

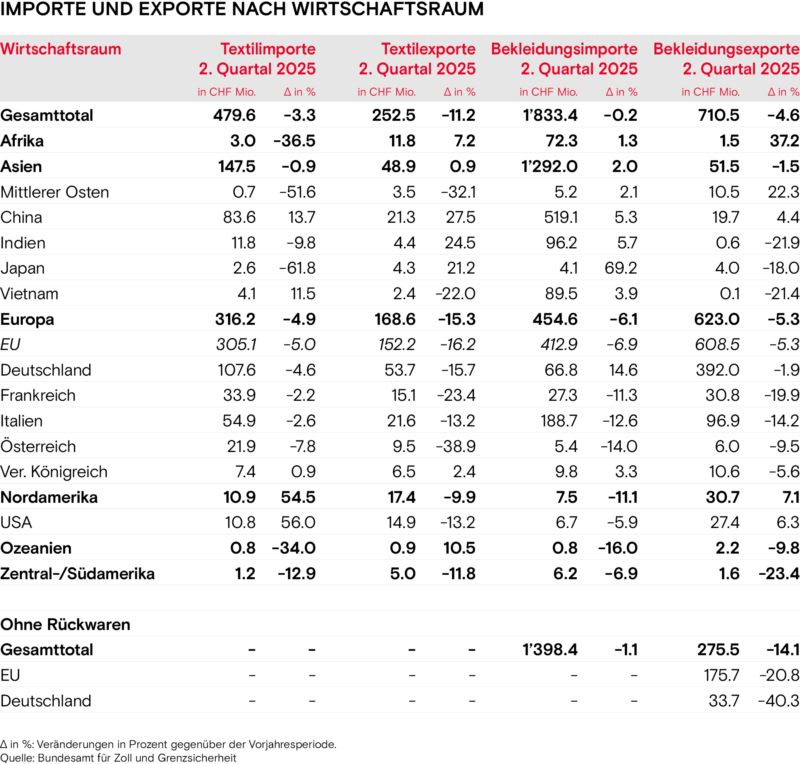

Foreign trade - focus on individual markets

Global uncertainty is reflected in the trade figures. Imports and exports fell in both the textile and clothing sectors compared to the previous year. This was most evident in exports of textiles and clothing excluding returned goods. The decline there is in the double-digit range.

In the case of textiles, it is related to the declines in the most important export groups - yarns, woven and knitted fabrics and technical textiles. There is less demand in Europe and the USA. Their sales figures already began to crumble in the first quarter.

The weakness in trade with the USA is likely to be largely due to the customs escapades. In the most important European market, Germany, sales remain low and the economic situation remains difficult. Only in Asia is demand increasing slightly, which is primarily linked to growth in China, India and Japan.

Clothing exports defy US tariffs

Here too, China is one of the few exceptions with a positive growth rate. Europe, on the other hand, is quite different. Germany in particular has less appetite for clothing from Switzerland. After deducting returned goods, exports to its northern neighbour fell by 40 percent.

Surprisingly, clothing exports to the USA also increased in the second quarter, mainly due to underwear. Sales had already increased in the low to mid double-digit percentage range in the previous quarters. However, the first tariff announcements dampened US consumers' desire to buy. With the newly imposed tariffs of 39 per cent, the trend is now likely to reverse completely.

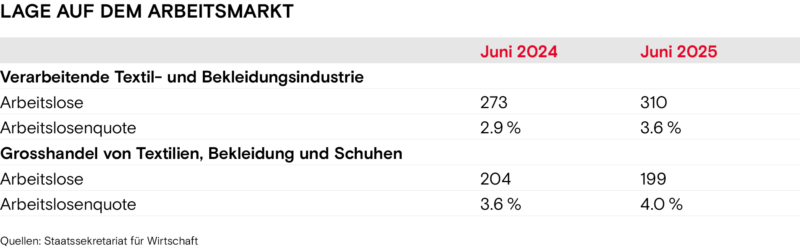

Situation on the labour market

The labour market is also feeling the effects of the current uncertain situation. The unemployment rate in the manufacturing textile and clothing industry as well as in wholesale increased compared to the previous year. This was particularly noticeable in the manufacturing industry with an increase of 0.7 per cent.

However, the textile industry is not the only sector affected by this development. The overall unemployment rate is 2.7 per cent, an increase of 0.5 per cent compared to the previous year.

Unemployment is likely to rise in the coming months, particularly in the manufacturing industry and in the clothing retail trade. Textile wholesalers are still a little more cautious here and the majority of companies expect the same number of employees in the next three months.

Outlook and expectations

The manufacturing industry is expecting a slight increase in orders. This is an important sign, as they were still expecting a decline at the beginning of the second quarter. Estimated exports are also showing a slightly positive trend.

Both wholesalers and the manufacturing industry are expecting prices to rise again after remaining rather stable in the first quarter. However, wholesalers are not expecting an upturn any time soon, with the balance of expected demand at practically zero.

Only the clothing retail sector is more optimistic. A small majority even expect sales to rise.

Export-orientated economy under pressure

Based on the survey prior to the tariff announcement, the figures are likely to deteriorate again in the coming months. Especially for companies in the sector that trade with the USA and produce in Switzerland. If they are unable to pass on the tariffs to their customers, they will have only two options: alternative production or a temporary delivery stop.

Bilateral III as a must-do

Agreements with other trading partners are therefore all the more important. And there are quite a few of them. The free trade agreement with India comes into force on 1 October and offers access to a new market. Those with Thailand and Malaysia are about to be debated in parliament. Another silver lining on the horizon is the conclusion of negotiations with Mercosur.

A little further away in terms of time, but crucial due to the geographical proximity to Switzerland, are the Bilateral Agreements III, which the Councils are expected to discuss in 2026. Stable and strong relations with Switzerland's most important partner are essential, especially in the current difficult global situation.