Economic report spring 2026

Starting 2026 with a headwind

The economic surveys for the first quarter of 2026 among companies in the Swiss textile and clothing industry continue to show a mixed picture. The outbreak of the war in Iran has dashed hopes of a rapid upturn. The outlook for the coming months is correspondingly cautious.

The situation looks familiar: Once again, the global situation has dampened the positive trends during the turn of the year. The situation was similar in 2025. Following the customs turbulence, the war in Iran is now making the first quarter more difficult.

In addition to the prevailing uncertainty, price increases in particular need to be kept in mind: Both raw materials and chemicals have become significantly more expensive in just a few weeks. Depending on how the situation develops, energy prices, for example, are also likely to rise further and make production more expensive.

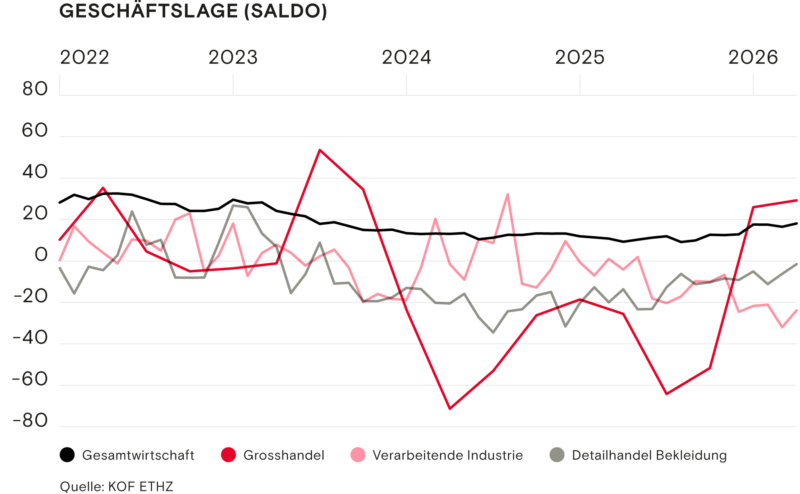

Manufacturing industry

The manufacturing industry in particular is feeling the effects of this, as the assessment of the business situation shows. Since the beginning of the year, the number of companies with a negative assessment of their situation has risen again. This is also reflected in capacity utilisation, which has fallen to below 74%. At the same time, a large majority of respondents expect prices to rise in the coming months. This is likely to put additional pressure on demand, which is already weak.

Wholesale

By contrast, textile wholesalers are far more optimistic: the majority now rate the business situation as good for the second time in a row after two poor years. Unlike the manufacturing industry, however, wholesalers expect prices to remain stable.

Retail trade

The textile retail trade is positioned between the wholesale trade and the manufacturing industry: the slightly positive trend of the past quarters is continuing. The balance is now only just in negative territory. If the trend continues, it could turn positive in the coming months.

The business situation represents the overall economic situation of the company. The test participants answer the question: "We currently rate the overall business situation as good, satisfactory or poor."

The companies' expectations mentioned below are based on various questions regarding the expected business situation, order situation or turnover in the next three to six months.

Here, too, there are three possible answers ("better", "neutral" and "worse"). Due to the slightly varying questions between the sectors, a direct comparison between the sectors is sometimes imprecise. However, the chart shows the trends in the coming months, which help with an assessment.

The seasonally adjusted balance of positive and negative responses is shown for the two indicators. This reflects the trend in development. In practice, the balances show a high correlation with the actual growth rates of the real indicators. The figures for positive and negative responses (percentages in the text) are not seasonally adjusted (source: KOF ETHZ).

in German only

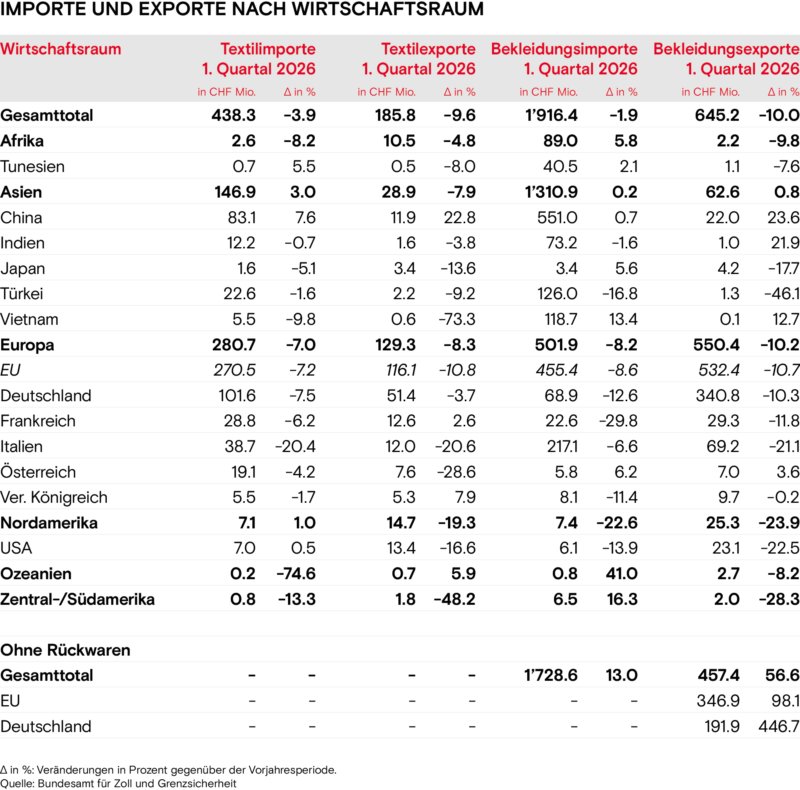

Foreign trade - focus on individual markets

Foreign trade has weakened significantly. Imports and exports fell in both the textile and clothing sectors compared to the previous quarter. Exports fell by around ten per cent. The reason for this is the continued weak demand in Europe and the USA.

Only Asia showed a positive trade balance, which is primarily due to China. Swiss textiles and clothing are particularly popular there and grew by over 20 per cent compared to the same quarter last year. Imports also increased, albeit at a slightly slower rate.

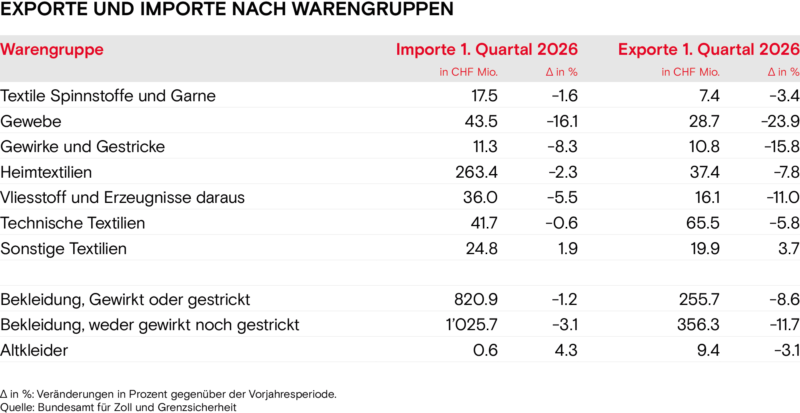

A look at the product groups shows: In the case of textiles, fabrics in particular are traded significantly less. The decline in both imports and exports is in the double-digit percentage range. Demand also fell for other important product groups such as technical textiles and home textiles.

Adjusted for returned goods, clothing exports recorded strong growth. This is due to the fact that significantly fewer returned goods were recorded, particularly in trade with Germany. Returned goods worth CHF 150 million were registered, compared to CHF 345 million in the same quarter of the previous year (-56 per cent). At the same time, exports to Germany fell by only CHF 40 million (-10 per cent). The BAZG is checking the data on this. They should therefore be viewed with caution at present.

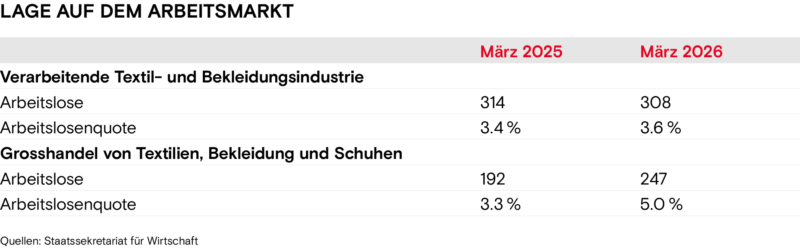

Situation on the labour market

The unemployment rate in the manufacturing industry increased slightly compared to the previous year and stood at 3.6 per cent in March 2026.

Wholesale suffered a larger increase and stands at 5 per cent. This trend is likely to continue in the coming months, as the companies surveyed expect the number of employees to fall slightly.

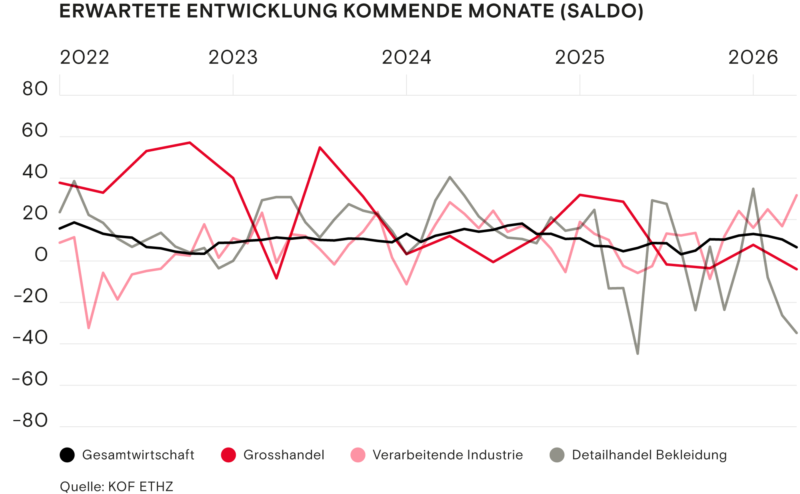

Outlook and expectations

Looking ahead, there are also clear differences between the sectors. The manufacturing industry ended the year with positive expectations and continued this trend in the first quarter. In March, the balance value reached more than 30 points - the highest level in recent years. One reason for this is the rise in export expectations.

The picture is different in the clothing retail sector. After peaking in December with a balance of plus 30 points, expectations turned significantly negative three months later: in March, they stood at minus 35 points. However, assessments have fluctuated greatly in recent months and the latest development fits in with this volatile picture.

The textile wholesale sector has a comparatively neutral outlook for the coming months. The Swiss economy as a whole presents a similar picture: its assessment is close to the long-term average.

Uncertainty makes forecasts difficult

The Swiss textile and clothing industry continues to feel the uncertainty caused by the geopolitical situation. Although it is not directly affected by the war in Iran, the indirect effects are also having an impact. Above all, the rising prices of raw materials and energy costs are likely to continue to affect the industry in the coming months.

In terms of domestic policy, decisive decisions will be made in the coming months. While the chaos initiative poses a serious threat to relations with the EU, several free trade agreements, such as with the Mercosur states and Malaysia, are in the process of being ratified by parliament. The opportunity to open up new markets could give the industry a new boost.