Economic report winter 2025/26

A year of extremes

Last year was an extreme year for the Swiss textile industry: additional US tariffs of 39 per cent and a strong Swiss franc had a massive impact. While textile exports slumped by 7.7 per cent, wholesalers and retailers showed the first positive signs towards the end of the year. With the US customs deal and the India free trade agreement, the industry is cautiously optimistic about 2026.

Customs hammer shakes the industry

As if the previous years had not already been challenging, US President Donald Trump made the situation even more difficult in 2025. With his announcement of reciprocal tariffs, he set a dynamic in motion that made waves around the world. Companies that were not focussed on the US market felt the effects of this in particular. Export-orientated companies were faced with major challenges. They had to react flexibly. The Swiss textile industry was no exception.

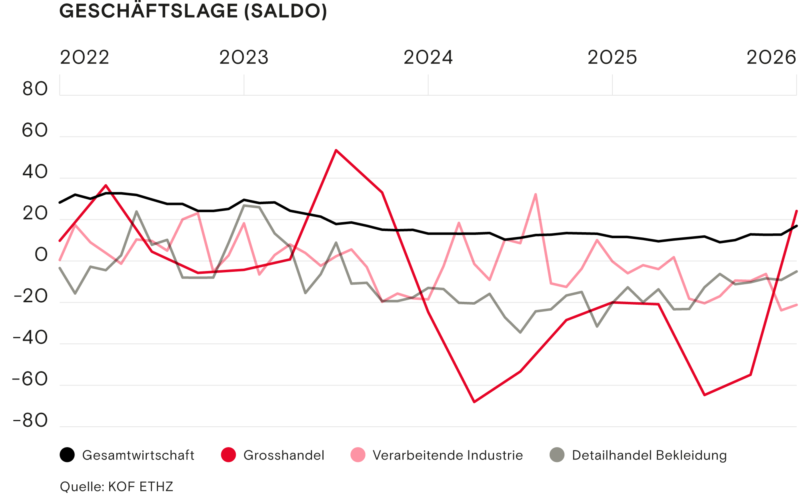

The development of the business situation in the textile wholesale sector clearly shows which topic set the pace last year: customs policy. In April, Trump announced new tariffs. He raised them again in the summer. The beginning of a slump became apparent. The tariff hammer in the summer hit the manufacturing industry particularly hard.

The mood brightened towards the end of the year. The textile wholesale and clothing retail sectors showed positive trends. Only the manufacturing industry continued to take a negative view of the situation.

More than a dozen companies had to close down

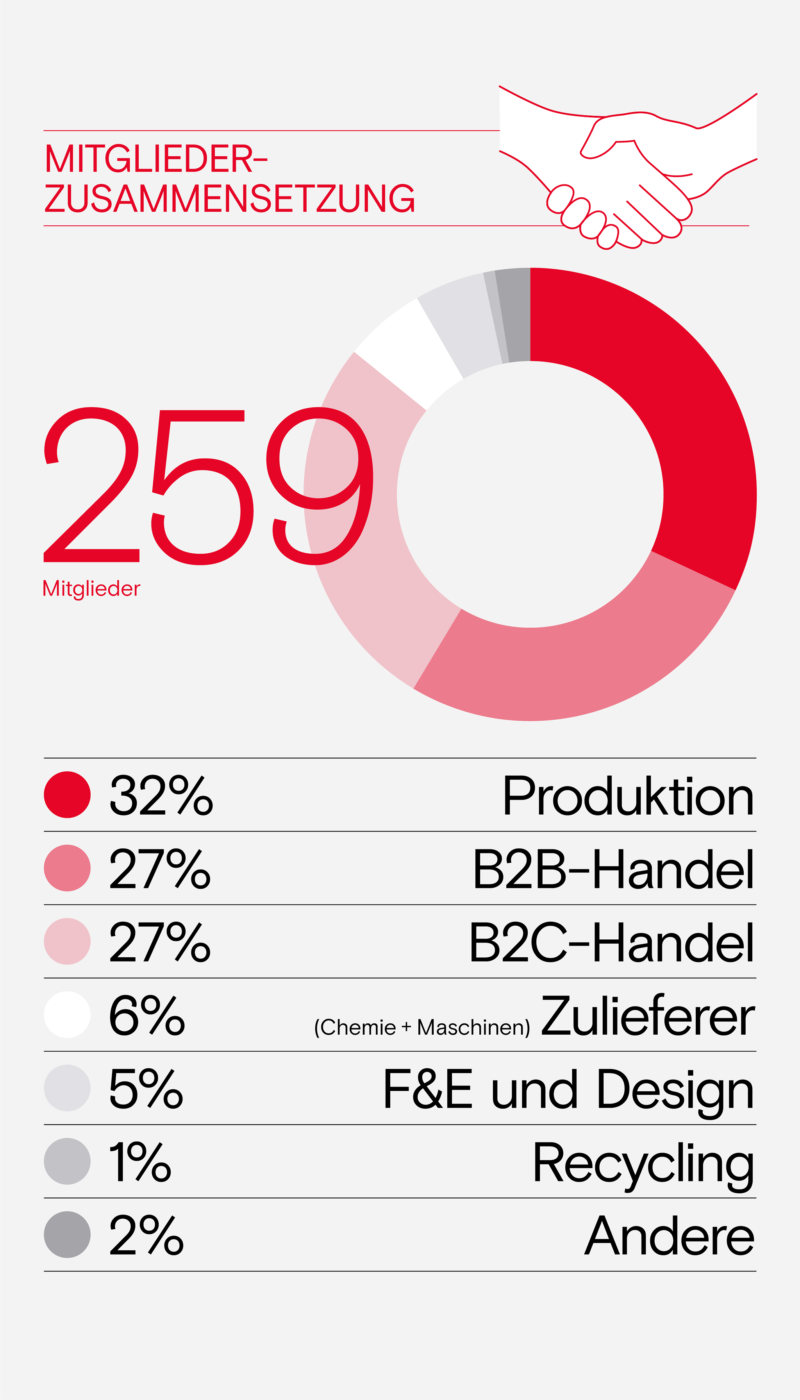

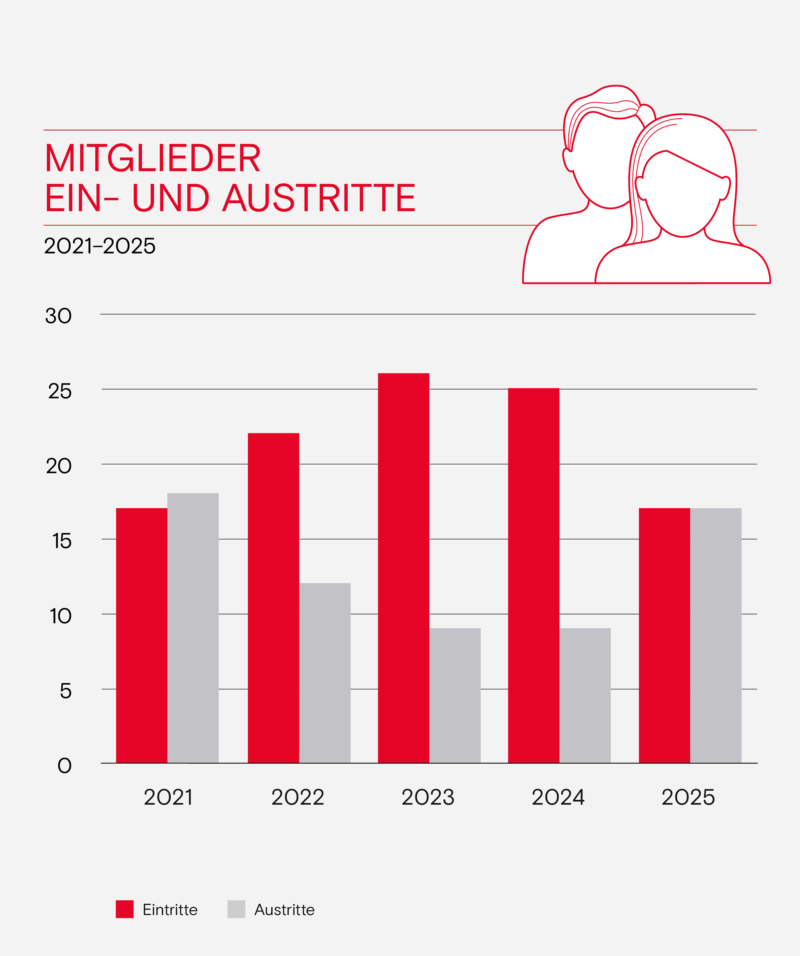

This development is reflected in the membership of Swiss Textiles. The number of members remained stable thanks to new memberships. However, more than a dozen companies had to cease their business activities. Particularly affected: industrial manufacturing companies in Switzerland. They now make up only a third of the members.

Swiss production struggles

The manufacturing industry has been under pressure for years. The pandemic, the war in Ukraine, rising energy prices and falling demand have all left their mark. The EU is trying to curb the excessive bureaucracy. At the same time, however, its protectionist measures are excluding Swiss producers.

However, the main perpetrator of this isolationist policy is in Washington. The announcement that Swiss goods would suddenly be subject to punitive tariffs came as a surprise to many companies. The introduction was postponed a short time later. However, the uncertainty remained.

Competitiveness was only restored to some extent with the conclusion of the deal with the USA. The damage had already been done by then.

39 per cent duty - no longer competitive overnight

The situation worsened dramatically in the summer. Trump announced a new tariff rate of 39 per cent. The problem: the difference to the most important competitors, above all the EU. Swiss companies lost their competitiveness practically overnight.

Competitiveness was only restored to some extent with the conclusion of the deal with the USA. The damage had already been done by then.

The franc becomes a burden

In addition to the tariffs, a second problem is weighing on the industry: the currency situation. The volatile situation caused the US dollar to lose confidence. The Swiss franc once again lived up to its reputation as a safe haven.

This is becoming a problem for internationally orientated Swiss companies. Many are invoicing in US dollars and budgeting in Swiss francs at the same time. They have to cope with massive losses in value.

Tariffs and industrial policy don't just harm individual countries. In the end, all market participants suffer.

A level playing field for all - more urgent than ever

Swiss Textiles already wrote about this a year ago: A level playing field for all is imperative. This demand has once again proven to be true.

Swiss suppliers are at a disadvantage in online trading. Foreign marketplaces benefit from regulatory loopholes. In international trade with the EU and the USA, protectionist measures are hampering business. Tariffs and industrial policy do not just harm individual countries. In the end, all market participants suffer.

Economic indicators: conciliatory end to the year

The fourth quarter ended on a conciliatory note. The free trade agreement with India came into force on 1 October - a positive start. The good news followed in mid-November: the customs deal with the USA was finalised. After the ups and downs of the previous months, this was a hopeful conclusion to a challenging year.

Manufacturing industry continues to struggle

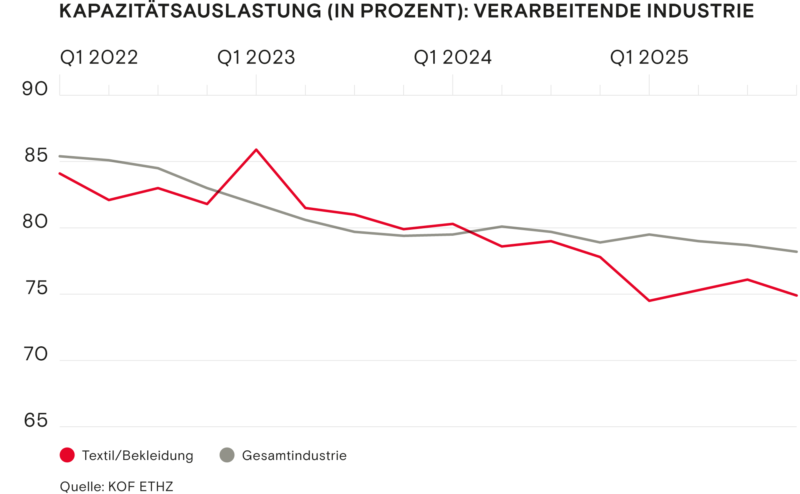

The manufacturing industry is still struggling. Companies rate both capacity utilisation and the order backlog as too low. In both areas, the textile industry is below the industry average for Switzerland as a whole.

The clothing retail sector has shown a positive trend since the beginning of the second half of the year.

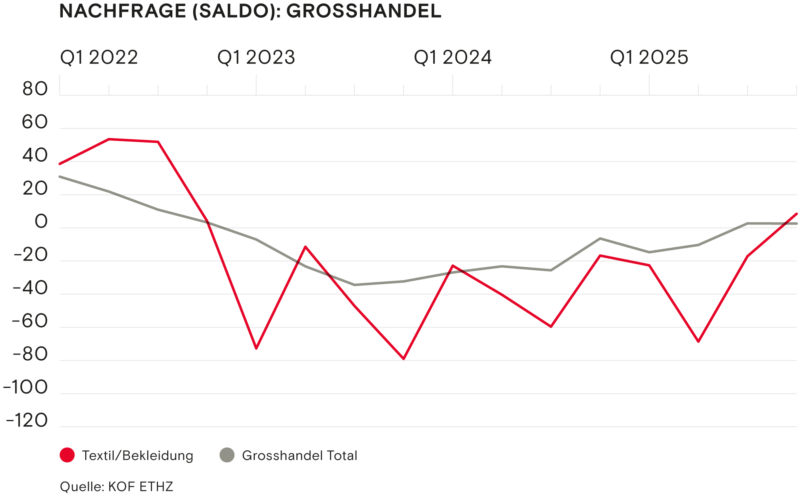

Wholesale: bright spot in the fourth quarter

The wholesale sector is more positive than the manufacturing industry. The reason: a successful last quarter. Wholesale also suffered from the difficult market situation over the course of the year. However, in the fourth quarter, the companies surveyed reported an increase in demand for the first time since 2022.

Positive trend in the clothing retail sector

The clothing retail sector has shown a positive trend since the beginning of the second half of the year. This trend was confirmed in the fourth quarter. The main reason for this is likely to be the improved consumer sentiment on the domestic market.

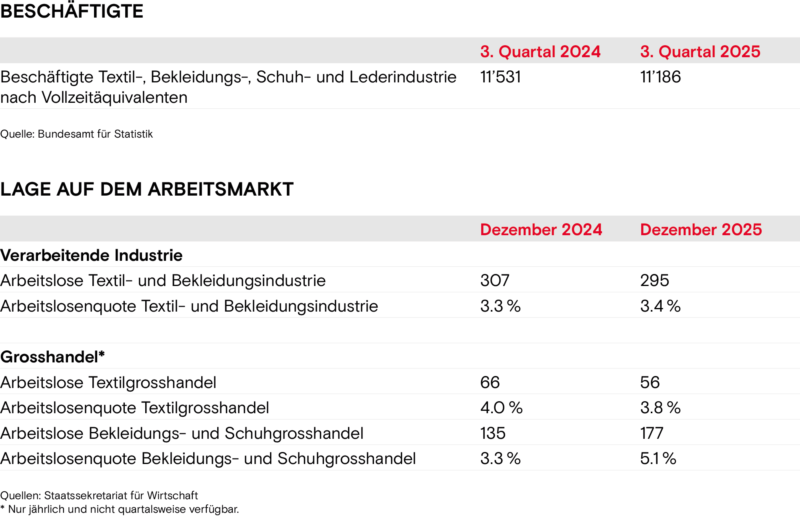

Labour market: stable, but under pressure

The unemployment rate in the manufacturing industry has hardly changed compared to the previous year. However, it remains above the national average. The situation is different in the wholesale sector, where the difficult year was also reflected in the unemployment rate.

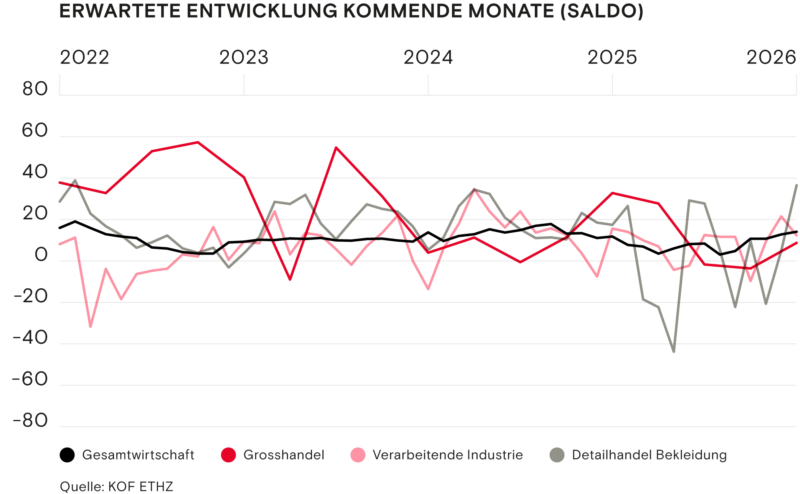

The assessment of the wholesale sector is particularly striking. After the slump in the middle of the year, it closed on a clearly positive note. The majority of retailers and the manufacturing industry moved sideways. However, the trends differ: the retail trade is showing a rising curve. The manufacturing industry, on the other hand, is less optimistic about the situation.

At the end of the pandemic, capacity utilisation was still at 85%. Since then, it has fallen steadily. At the end of 2025, it reached 75 per cent. Swiss industry as a whole was slightly higher at 78 per cent.

The reason for the more positive mood among textile wholesalers is reflected in the demand figures. For the first time since 2022, a small majority reported an increase in demand over the past three months.

The business situation represents the overall economic situation of the company. The test participants answer the question: "We currently rate the overall business situation as good, satisfactory or poor." The order backlog comprises the quantity or value of customer orders not yet in progress. The test participants answer the question: "Overall, we rate the order backlog as large, normal, too small." Demand comprises the demand for services in Switzerland and abroad. The test participants answer the question: "Demand for our services has risen, remained the same or fallen in the last three months."

The seasonally adjusted balance of positive and negative answers is shown for the four indicators. This reflects the trend in development. In practice, the balances show a high correlation with the actual growth rates of the real indicators. The figures for positive and negative responses (percentages in the text) are not seasonally adjusted. (Source: KOF ETHZ)

Employment: 11,000 jobs in manufacturing

The manufacturing industry still employed 11,186 full-time equivalents in 2025. This is significantly below the previous year's level. Strikingly, the unemployment rate remained relatively stable at 3.4 per cent. This means that laid-off employees found jobs in other sectors.

The unemployment rate fell slightly in textile wholesale. In clothing wholesale, however, the labour situation deteriorated.

Outlook: Further job cuts expected

The situation is unlikely to improve in the coming months. Both wholesalers and the manufacturing industry are cautious and expect employment figures to fall.

Foreign trade

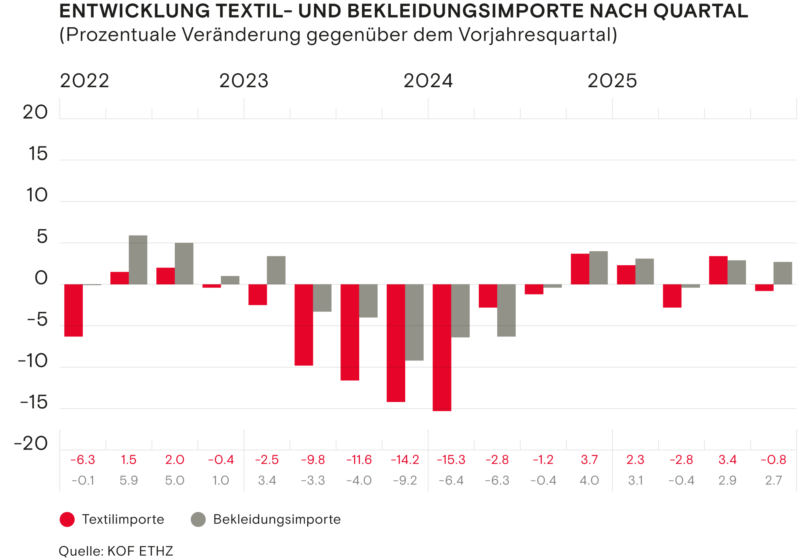

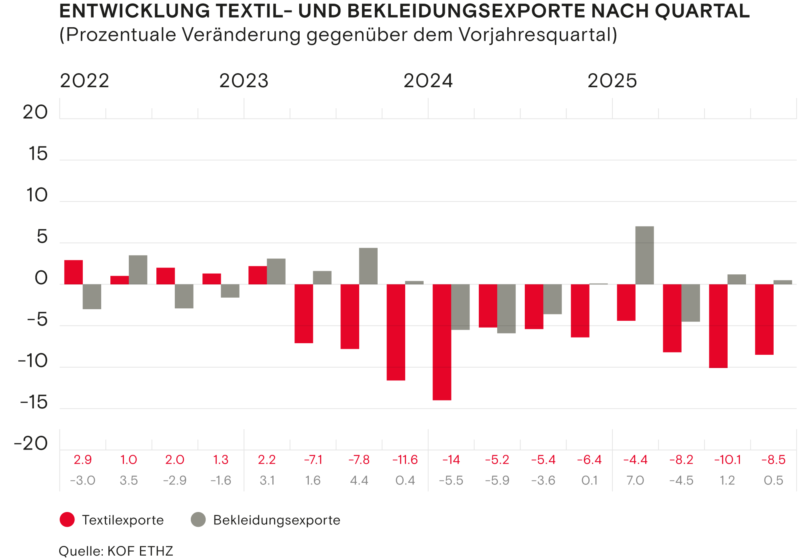

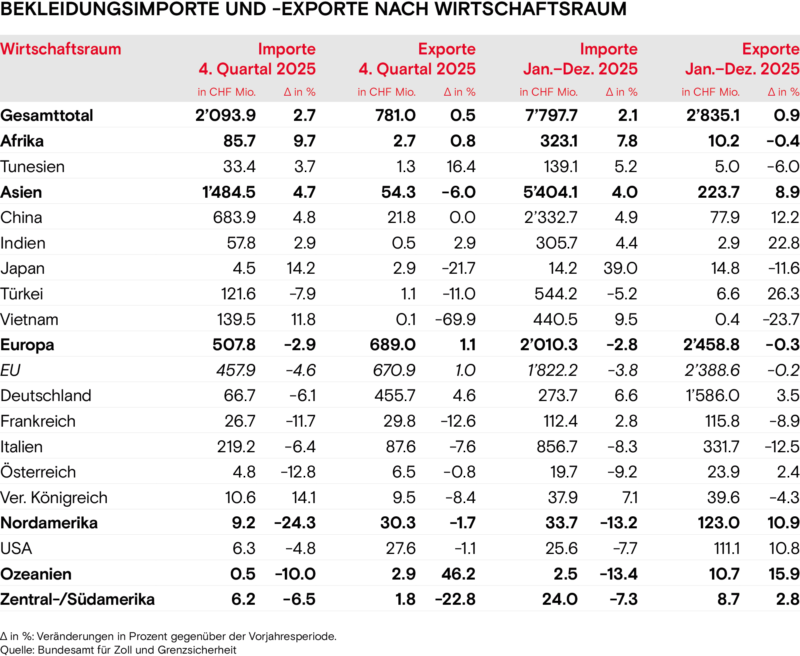

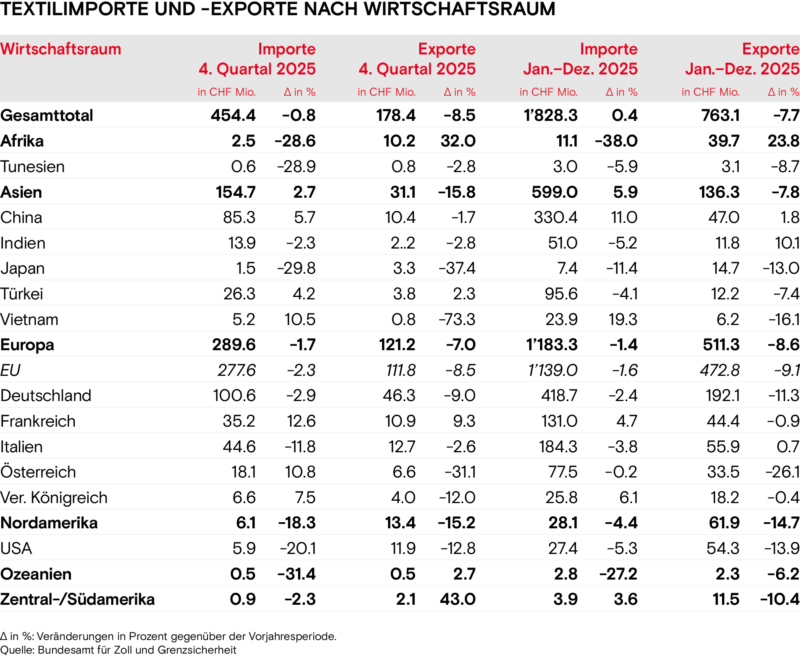

Trade data in the clothing sector remained relatively stable and even grew slightly. The situation was different for textiles: demand from abroad collapsed. Exports fell by 10 per cent in the third quarter. In the fourth quarter, the decline was still 8.5 per cent.

Textile imports developed more positively. They recorded slight growth in two quarters.

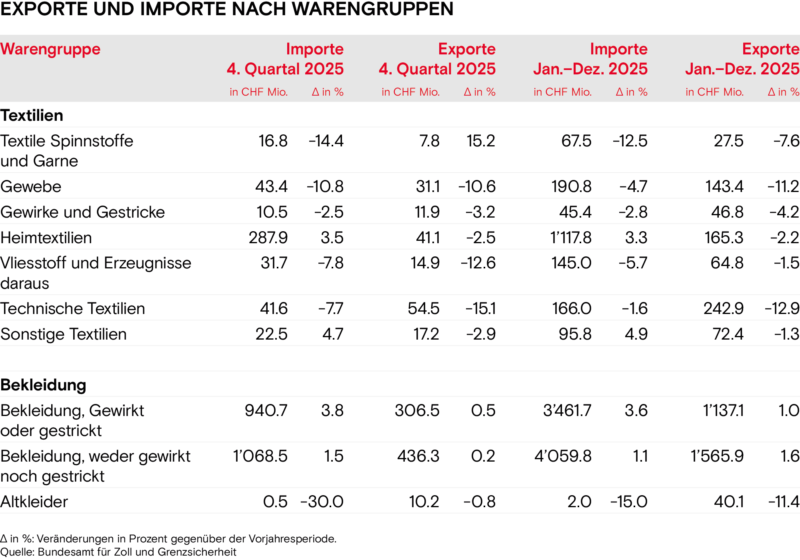

Technical textiles: down 15 per cent

Technical textiles recorded the sharpest decline in exports in the fourth quarter: minus 15 per cent. Nonwovens and woven fabrics also fell significantly. Home textiles performed better with a drop of 2.6 per cent. Textile spun fabrics and yarns even increased by 15 per cent.

Africa saw strong demand for Swiss textiles. And the Middle Kingdom recorded growth in both imports and exports over the year.

Imports: reverse picture

The picture was reversed for imports. There was less demand for spun fabrics and yarns. Home textiles, on the other hand, recorded increased domestic demand.

Countries: EU, Asia and USA are weakening

The EU, most Asian countries and - unsurprisingly - the USA were primarily responsible for the decline in imports and exports.

Two positive exceptions stand out: Africa showed strong demand for Swiss textiles. And China bucked the trend. The Middle Kingdom recorded growth in both imports and exports over the year.

Clothing: Stable trade with moderate growth

The clothing sector proved to be much more stable than textiles. Imports and exports only fell slightly in the second quarter. In the remaining quarters, trade figures grew compared to the previous year. Growth rates remained in the low single-digit range - with one exception: clothing exports rose sharply in the first quarter.

Knitted and woven clothing on the rise

Exports of knitted and crocheted clothing and woven garments increased by around one per cent in the last quarter and over the year as a whole. However, growth declined slightly in the fourth quarter.

Knitted and crocheted clothing was more popular and grew by over 3.5 per cent in the last quarter and over the year as a whole compared to the previous year.

Home textiles: particularly popular in Germany

Other ready-made goods such as bed linen and blankets were in greater demand domestically. However, exports fell in comparison to the previous year.

Germany remains the most important trading partner within the EU. Its importance for Swiss clothing exports became clear once again.

USA surprises with export growth

The main driver of the positive trend in imports is the Asian region, above all China. However, the volume of imports increased significantly more than their value. The volume grew by 14 per cent, the value by just under 5 per cent. This indicates that Asian online marketplaces are continuing to gain ground.

Germany: most important EU partner strengthened

Germany remains the most important trading partner within the EU. Its importance for Swiss clothing exports became clear once again - a success after the difficult past few years. Although this is just the beginning.

USA paradox: growth despite punitive tariffs

The USA is also experiencing export growth. This is surprising. After all, Switzerland's additional tariffs were among the highest in the world. A decline would have been expected.

The explanation is relatively simple: the vast majority of clothing is not produced in Switzerland. The decisive production steps do not take place in this country. In terms of customs law, the clothes are therefore not domestic goods. This is why the Swiss additional duty does not apply.

The situation is different for textiles. There has been a decline in exports to the USA.

The respondents agree on this. The economy is moving towards the end of the trough.

Cautious optimism for 2026

The companies surveyed have started the new year optimistically. The majority expect an improvement in all sectors. This applies not only to the textile and clothing industry, but also to the economy as a whole.

The manufacturing industry is expecting more orders again in the coming months. Export orders should also increase slightly. Wholesalers are anticipating increased demand. Companies in both sectors expect prices to remain stable or increase slightly.

Retail figures: cautious trend in the fourth quarter

The respondents agree on this. The economy is moving towards the end of the trough.

Trade figures were rather cautious in the fourth quarter. Exports were somewhat weaker compared to the year as a whole. However, there were no sharp fluctuations.

Geopolitics remain unsettling

Global politics remain uncertain. 2025 clearly demonstrated how quickly the situation can change completely within a few days. Companies must remain flexible in order to be able to react to such external shocks.

Swiss companies need a healthy domestic market climate so that they can concentrate on their core business.

Bright spots: India and Mercosur

The new free trade agreement with India developed favourably. It came into force on 1 October and is likely to shape the coming years. The same applies to the agreement with the Mercosur states. It opens up an important market that was previously sealed off with tariffs of up to 30 per cent.

Fair rules of the game required at home

In order for Swiss companies to be able to concentrate on their core business, they need a healthy domestic market climate. This means a level playing field for all. Applicable law must apply to everyone - especially in online trading.

It is also important that relations with the USA are stabilised. Broad-based trade relations are crucial for our global industry. We clearly reject protectionist measures and call for open trade relations on an equal footing

Working together with Europe

The bilateral approach with the EU must be continued. The Bilaterals III are essential in order to stabilise and further develop the relationship with the EU. In challenging times, cooperation is a must.